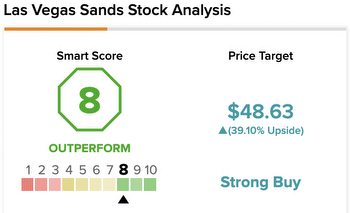

Smartkarma questions S&P decision to downgrade Las Vegas Sands to junk

$5,000 Welcome Bonus

Investment insights platform Smartkarma has questioned a decision by S&P Global Ratings to cut global casino giant Las Vegas Sands to junk, claiming it paints an overly negative picture of the company’s solvency and the recovery outlook of its key markets in Macau and Singapore.

S&P issued the downgrade last week, dropping LVS to below investment grade at “BB+” due to a slower than expected recovery in Macau as a result of the global Omicron outbreak. The ratings agency remains the only one to have issued such a downgrade at this stage, with both Moody’s Investors Service and Fitch Ratings holding firm.

In a Tuesday note, Smartkarma’s Howard J Klein said it is “hard to fathom” why S&P felt the need to issue a downgrade at this time given the overly negative picture even a modest debt downgrade can paint of a company’s solvency outlook as a result of subsequent media coverage.

“Those who may recall the 2008 global financial meltdown was linked to the contagion of mortgage collateralized bonds failing en masse. Among those many culprits creating the crash were the rating services which had rated tranche after tranche of bonds with high-risk mortgages buried within the solid ones,” Klein said.

“Since then the ratings industry has scrupulously observed every fire wall imaginable to keep the ‘purity’ of their ratings systems free of taint. That’s the good news. But what hasn’t changed is the headline impact of both upgrades and downgrades on the common.”

While Klein acknowledged that alerting lenders and debt holders to increased risk is part of S&P’s mission, he suggested that news regarding more bullish outlooks for LVS had “fallen between the cracks” for many investors.

Pointing to S&P’s projections, which have Macau-wide GGR reaching between 30% and 40% of 2019 levels, Klein said LVS still appears to be in good shape with a US$1.64 billion current cash position – set to be boosted by the sale of its Las Vegas assets this year – and “a steady shrinkage of operating losses from Macau and Singapore” in recent quarters.

As a result, Smartkarma has “stuck to our high conviction bull scenario for LVS for reasons that show connective tissue between the company’s outlook in the near as well as out-year performance.”

The platform outlined a series of key reasons behind its more positive view of LVS, including the ability to easily recoup the 11% contribution to group-wide EBITDA from its former Las Vegas assets, positive signs from the Macau government around concession renewal terms, solid projections from analysts and evidence that LVS was well-placed to win a high-profile court case against a former partner currently taking place in Macau.

With this in mind, “it is hard to fathom why at this time S&P believed a downgrade was in order,” Klein said.