Are These 3 Casino Stocks a Good Buy Now?

$6,000 Welcome Bonus

Casino stocks can be a lucrative opportunity for investors with a high risk appetite. Casinos have enormous growth potential, as they often benefit from increased during good economic times. Furthermore, the rise of online gambling and has provided exciting new revenue streams for traditional casino operators.

The post-pandemic market is showing significant recovery and growth in the hospitality and entertainment sectors, as have increased foot traffic and occupancy rates in hotels with casinos. Let’s take a look at these three casino stocks that Wall Street believes are strong buys, and could rally around 30% to 45% in the next 12 months.

#1. MGM Resorts International

Headquartered in Las Vegas, MGM Resorts International MGM operates a diverse portfolio of hotels, casinos, and entertainment venues. The company's flagship properties include the Bellagio, MGM Grand, and Mandalay Bay in Las Vegas, as well as other well-known resorts in Macau and other destinations. Plus, the company also ventured intoU.S. sports betting and online gaming through BetMGM.

Valued at $13.3 billion, the stock is down 3.1% in 2024, compared to the S&P 500 Index’s SPX gain of 16.1%.

The company's portfolio includes 31 distinct hotel and gaming destinations worldwide. MGM's revenue fell during the pandemic, but recent quarters have shown signs of improvement.

In the recent first quarter, revenue increased by 13% to $4.4 billion. Consolidated adjusted EBITDAR landed at $1.2 billion, with 68% growth in adjusted net earnings. Casinos use EBITDAR as a financial performance metric that excludes non-recurring or highly variable rent or restructuring expenses. It is derived by adding restructuring/rental costs to EBITDA (earnings before interest, taxes, depreciation, and amortization). Analysts predict that MGM’s earnings will increase by 3.2% in 2024, with further improvement by 15.7% in 2025, respectively.

In 2022, MGM China won a 10-year gaming license in the Chinese gambling hub of Macau, implying continued growth in the gaming industry. MGM’s prospects appear promising, given the ongoing recovery in the tourism sector and the company's strategic initiatives.

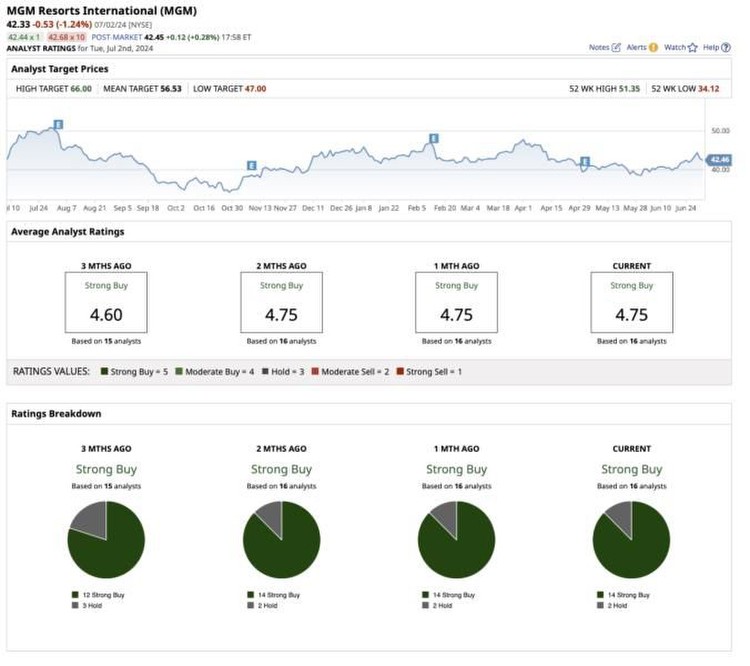

Overall, Wall Street rates MGM stock as a "strong buy." Out of the 16 analysts covering MGM stock, 14 recommend it as a "strong buy," and two rate it a “hold.”

Analysts' average price target of $56.53 suggests the stock can rise by 30.6% from its current levels. However, the high target price of $66 implies a potential 52.5% gain over the next year.

#2. Wynn Resorts

Las Vegas-based Wynn Resorts WYNN is a globally renowned operator of luxury hotels and casinos. Its flagship properties include the Wynn Las Vegas, Encore Las Vegas, and Wynn Macau. Valued at $9.6 billion, Wynn's stock is down 4.2% this year to lag the overall market.

Like MGM during the pandemic, Wynn Resorts experienced significant revenue decline and losses, resulting in increased debt levels. While the reopening of properties and increased visitation are benefiting the company, Wynn has yet to recover fully. At the end of the first quarter, total current and long-term debt was $11.2 billion, with cash and cash equivalents totaling $2.42 billion.

However, the global recovery of the travel and tourism industry, as well as the boom in digital gaming and online sports betting, could help the company reduce its debt burden.

In the first quarter, consolidated revenue rose 30.9% year over year to $1.86 billion. Adjusted net income increased dramatically to $1.59 per share, up from $0.29 per share in the year-ago quarter. The consolidated adjusted property EBITDAR increased to $646.5 million from $216.8 million in Q1 2023. Overall, the company reported a very successful quarter. Analysts covering WYNN stock expect its revenue and earnings to increase by 12.1% and 39.9%, respectively, for the full year 2024.

Overall, Wall Street rates WYNN stock as a "strong buy." Out of the 14 analysts covering Wynn, 13 recommend it as a "strong buy," and three rate it a “hold.”

Analysts' average price target of $123.86 suggests the stock can rise by 41.9% from its current levels. Plus, the high target price of $138 implies a potential 58.1% gain over the next year.

#3. Caesars Entertainment

Caesars Entertainment CZR is renowned for its iconic casino brands and extensive portfolio of resorts and properties. Its key properties includes Caesars Palace, Harrah’s, and Horseshoe, among others.

Valued at $8.09 billion, CZR stock is down 19.5%, compared to the broader market's double-digit gain.

In the first quarter, GAAP (generally accepted accounting principles) revenue came in at $2.7 billion, compared to $2.8 billion from the year-ago quarter. The company recorded a GAAP net loss of $158 million, versus $136 million in the prior-year quarter.

At the end of Q1, Caesars had cash and cash equivalents of $726 million. Its debt-to-equity ratio is quite high, at 2.67. However, Caesars Entertainment holds a strong market position with a well-recognized brand and a vast portfolio of properties.

Recently, Caesar completed the acquisition of WynnBET’s Michigan iGaming business operations. The company believes this deal will boost its “iCasino Net Revenue growth in an EBITDA accretive manner.”

The recovery of the tourism and gaming industries is another critical driver for Caesars Entertainment. Increased travel, higher hotel occupancy rates, and strong gaming activity are expected to boost revenue, allowing the company to turn losses into profits. Analysts who cover the stock expect it to earn $0.02 per share in 2024, with earnings increasing to $1.78 per share in 2025.

Overall, Wall Street rates CZR stock as a "strong buy." Out of the 16 analysts covering CZR, 12 recommend it as a "strong buy," and four rate it a “hold.”

Analysts' average price target of $54.44 suggests the stock can rise by 44.3% from its current levels. Furthermore, the high target price of $70 implies a potential 85.5% gain over the next year.

The Key Takeaway

Casino stocks can provide attractive growth opportunities, particularly as online gambling expands and the tourism industry recovers. I agree with Wall Street's positive outlook for MGM, WYNN, and CZR. They do, however, carry a higher risk of regulatory changes, economic sensitivity, and intense competition. Investors should conduct due diligence and assess their risk tolerance before investing in these three casino stocks.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.